CIFRS 16 - 1

CIFRS 16 introduces a single lessee accounting model and requires a lessee to recognise assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value. A lessee is required to recognise a right-of-use asset representing its right to use the underlying leased asset and a lease liability representing its obligation to make lease payments.

CIFRS 15 - 2

CIFRS 15 establishes the principles that an entity applies when reporting information about the nature, amount, timing and uncertainty of revenue and cash flows from a contract with a customer. Applying CIFRS 15, an entity recognises revenue to depict the transfer of promised goods or services to the customer in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

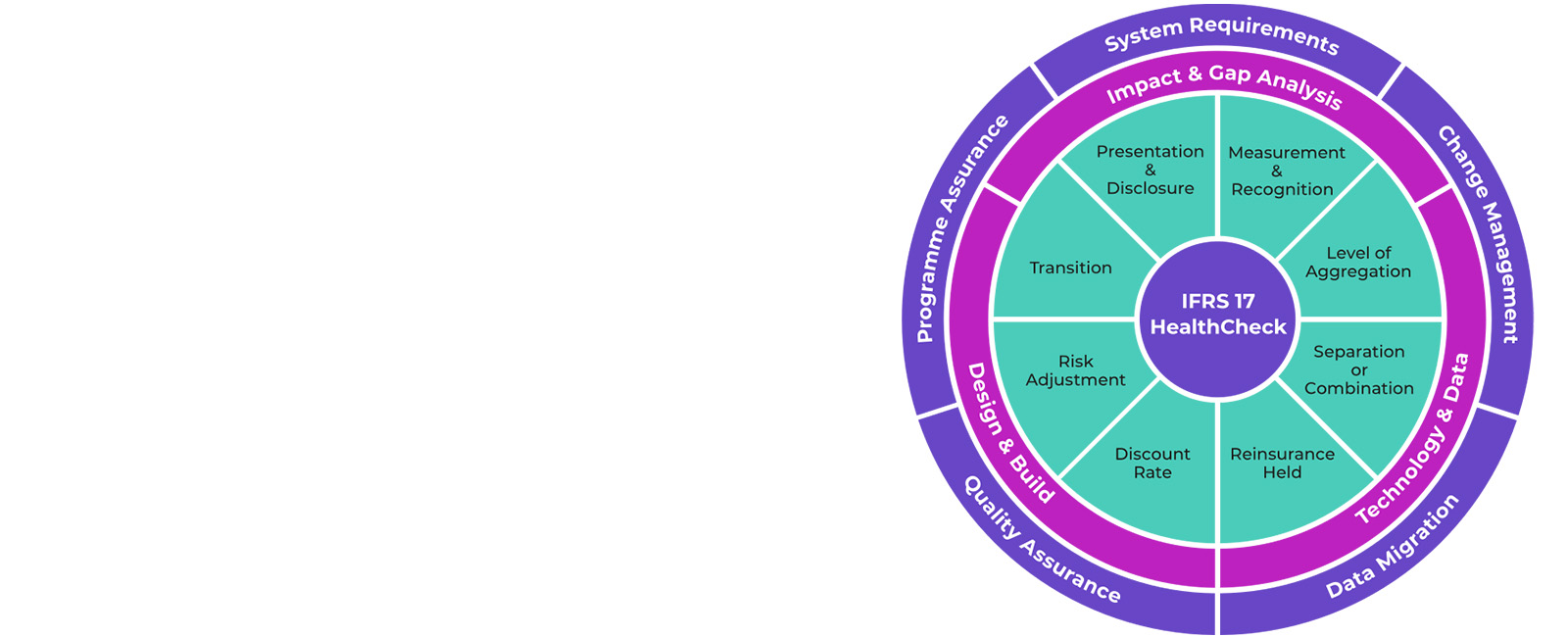

CIFRS 17 - Insurance contract liabilities

To provide useful information about these features, CIFRS 17: - combines current measurement of the future cash flows with the recognition of profit over the period that services are provided under the contract; - presents insurance service results (including presentation of insurance revenue) separately from insurance finance income or expenses; and - requires an entity to make an accounting policy choice of whether to recognise all insurance finance income or expenses in profit or loss or to recognise some of that income or expenses in other comprehensive income.

CIFRS 17 - Insurance contract liabilities

To provide useful information about these features, CIFRS 17: - combines current measurement of the future cash flows with the recognition of profit over the period that services are provided under the contract; - presents insurance service results (including presentation of insurance revenue) separately from insurance finance income or expenses; and - requires an entity to make an accounting policy choice of whether to recognise all insurance finance income or expenses in profit or loss or to recognise some of that income or expenses in other comprehensive income.

CIFRS 17 - Insurance contract liabilities

Insurance contracts combine features of both a financial instrument and a service contract. In addition, many insurance contracts generate cash flows with substantial variability over a long period.

CIFRS 19 - Financial instruments

CIFRS 9 requires recognition of impairment losses on a forward-looking basis, which means that impairment loss is recognised before the occurrence of any credit event. These impairment losses are referred to as expected credit losses (‘ECL’). In general, impairment losses are recognised on receivables, loan commitments and financial guarantee contracts

CIFRS 19 - Financial instruments

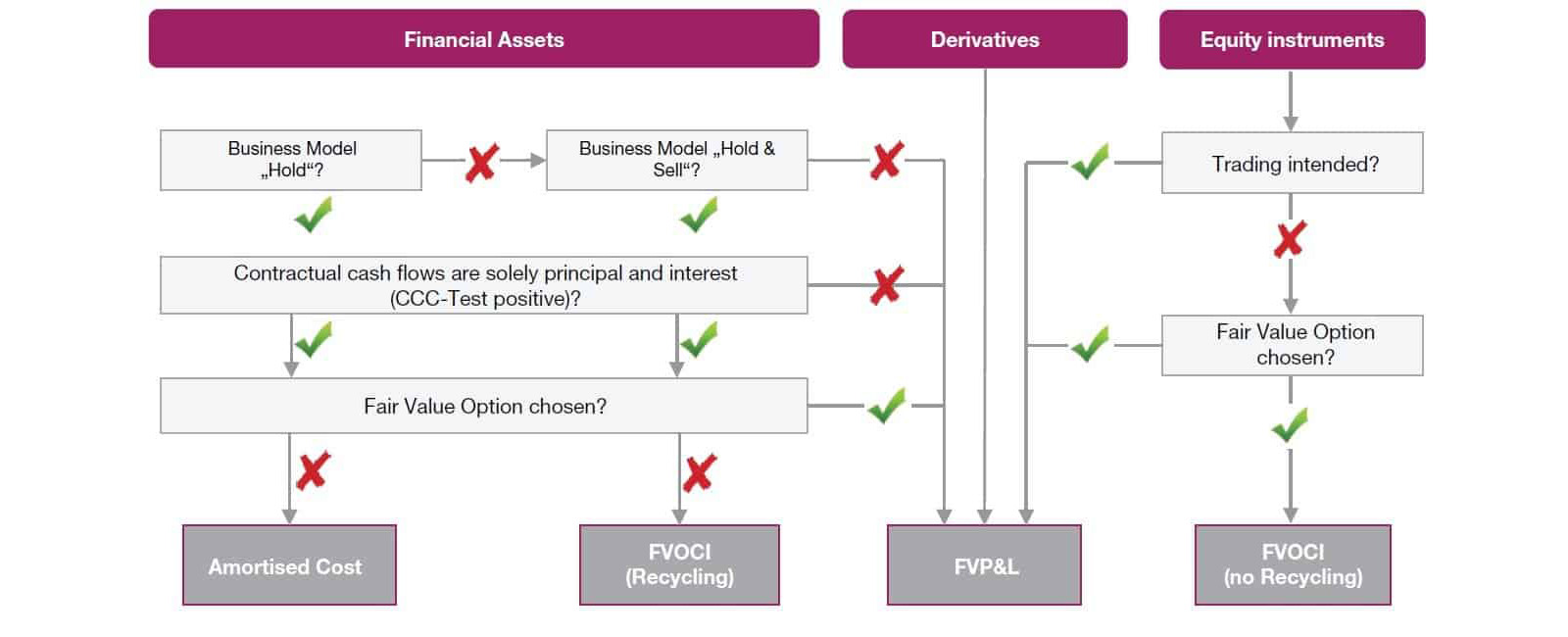

CIFRS 9 specifies how an entity should classify and measure financial assets, financial liabilities, and some contracts to buy or sell non-financial items. CIFRS 9 requires an entity to recognise a financial asset or a financial liability in its statement of financial position when it becomes party to the contractual provisions of the instrument. At initial recognition, an entity measures a financial asset or a financial liability at its fair value plus or minus, in the case of a financial asset or a financial liability not at fair value through profit or loss, transaction costs that are directly attributable to the acquisition or issue of the financial asset or the financial liability.

CIFRS 19 - Financial instruments

CIFRS 9 specifies how an entity should classify and measure financial assets, financial liabilities, and some contracts to buy or sell non-financial items. CIFRS 9 requires an entity to recognise a financial asset or a financial liability in its statement of financial position when it becomes party to the contractual provisions of the instrument. At initial recognition, an entity measures a financial asset or a financial liability at its fair value plus or minus, in the case of a financial asset or a financial liability not at fair value through profit or loss, transaction costs that are directly attributable to the acquisition or issue of the financial asset or the financial liability.

Cambodian International Financial Reporting Standards

Cambodian International Financial Reporting Standards (CIFRS) are a set of accounting standards that govern how particular types of transactions and events should be reported in financial statements.

International Financial Reporting Standards (CIFRS) are a set of accounting standards that govern how particular types of transactions and events should be reported in financial statements. They were developed and are maintained by the International Accounting Standards Board (IASB). The IASB’s objective is that the standards be applied on a globally consistent basis to provide investors and other users of financial statements with the ability to compare the financial performance of publicly listed companies on a like-for-like basis with their international peers. CIFRS are now used by more than 100 countries, including the European Union and by more than two-thirds of the G20

iN THE KNOW

Practitioner

We give solutions: Solution are refined and proposed to the best and most possible outcome, from calibrating scenario, understanding Project Manager’s concerns, and confirming project outcome (expectation from Project Manager).

We stand for simplicity: We understand barriers of great details to top Executives, and thus adopting outlook of the deliveries to Project Manager’s or entrepreneur’s needs and transform into more generic.

We do amazing projects: General projects (e.g. Bookkeeping, Reporting, and Taxation) are delivered diligently and prudently, while specalised projects (e.g. fund raising, business plan, and CIFRS conversion) are genuinely planed, executed, monitored, and concluded. We delivered what we promised.

We do it on time: We are embedded with professional commitment and have accomplished series of project without complaint of timeline. Our team knows exact consequence of missing deadline. Project Manager is constantly kept informed of project progress.

Our Services

We are Driven by Creating Experiences that Deliver Results for your Business and for your Consumers.

All ServicesCIFRS Conversion

Assessment, Progress, Knowledge Transfer, and First Time Adoption.

Financial Reporting

To record, process, and report of business-related transactions.

Taxation

To provide trusted services and become your primary consultant or tax agent.

Management Accounting

To organize and analyze cost center, revenue center, and profit center and report customization.

Assurance and audit

financial audit for being compliant with regulator, quarterly review, internal audit (project, department, internal process).

Credit Scoring

Fitted for CIAS 39 (incurred losses impairment) and CIFRS 9 (ECL) incorporating forward looking information, deriving from parametric statistical technique and supported hypothetical testing. Indicators are prudential selected and tested.

Impairment for CIAS 39 & CIFRS 9

Complete elements of EAD, PD, LGD, Discount rate, for individual and collective.

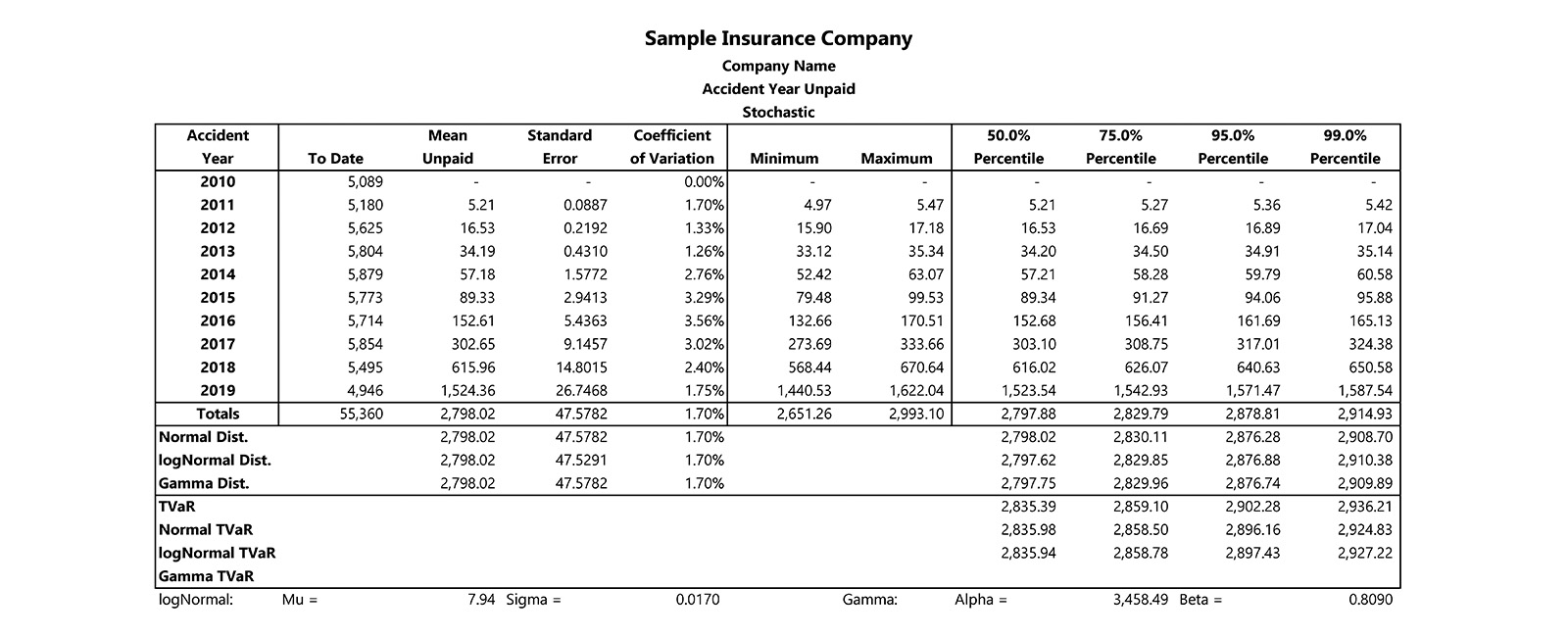

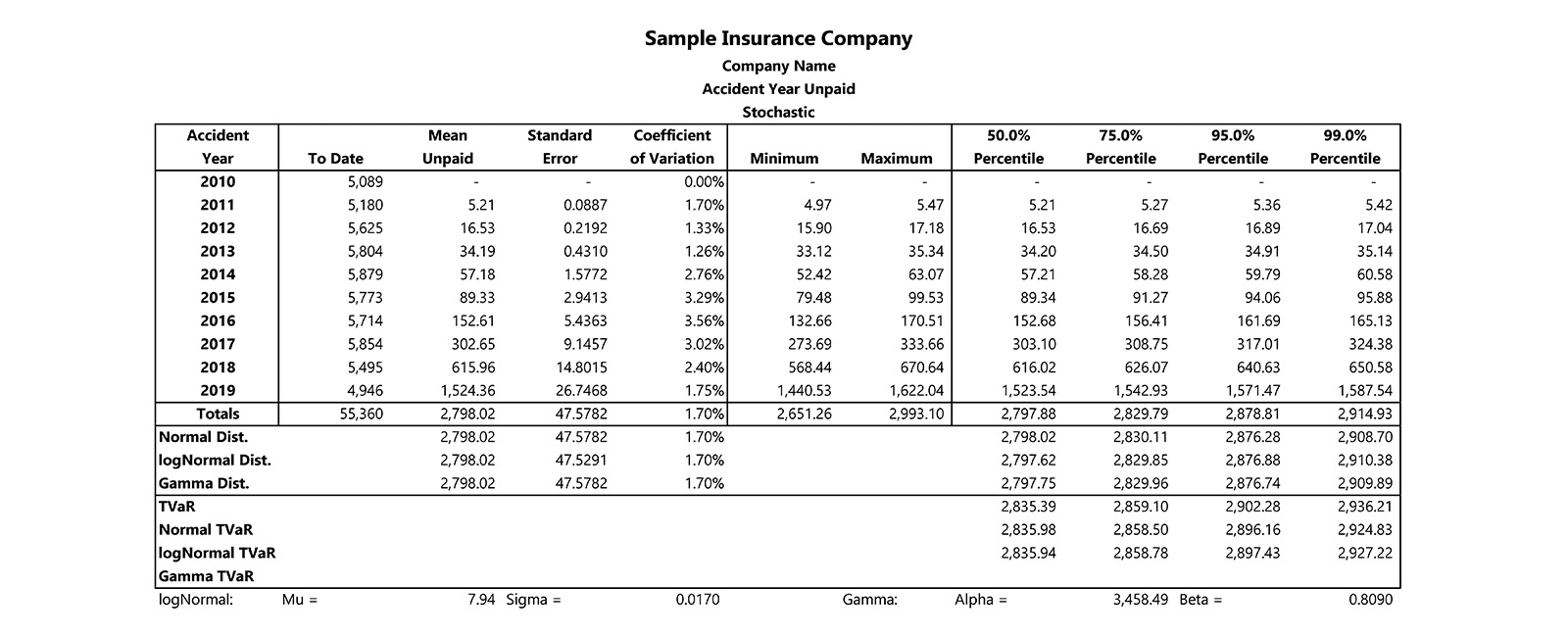

Insurance Contract Liabilities

incurred and reported, incurred but not reported, incurred but not sufficiently reported, provision for adverse deviation, unexpired risk reserve by deploying quantile technique and stochastic.